In volatile markets, the strongest opportunities are often not the loudest names, but those where fundamental quality is improving faster than the market is pricing it. LLB fits that profile.

From a fundamental factor perspective, LLB stands out as a high-quality regional financial institution: Tier 1 capital ratio of 19.0%, Liquidity Coverage Ratio of 149.9%, Net Stable Funding Ratio of 156.5%, leverage ratio of 6.7%, and a conservative loan-to-deposit ratio of approximately 80%. These are the hallmarks of a balance sheet designed to absorb stress rather than amplify it. Asset quality remains robust, with Stage 3 loans at roughly 1.0% of gross loans, comfortably below broader European banking system averages, while profitability remains resilient with ROE at 7.3%, despite a softer interest-rate environment.

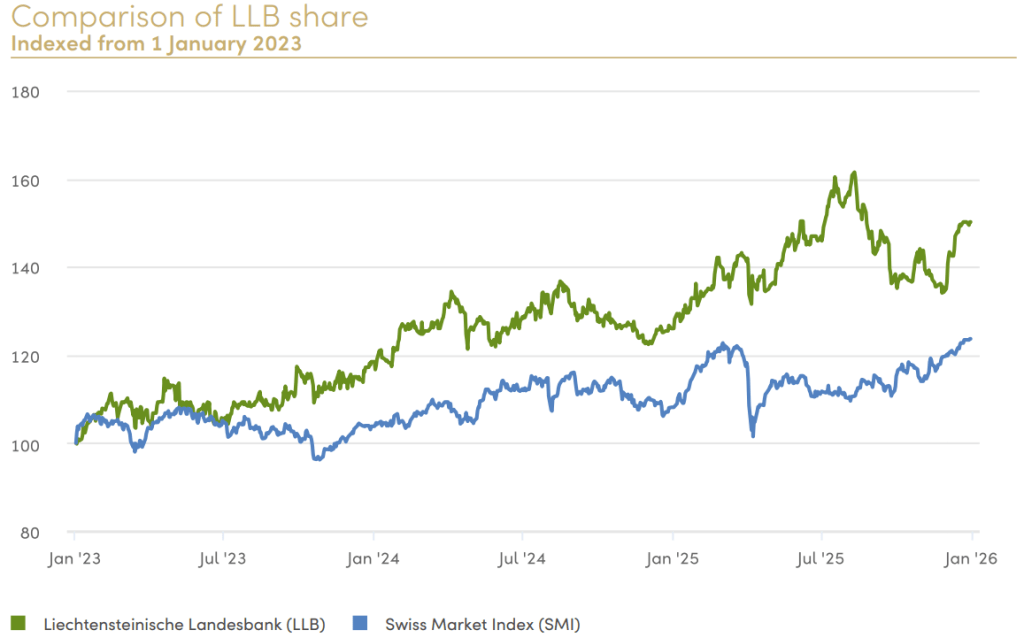

From a technical and market-structure perspective, the signal is also constructive. The stock delivered a 23.7% total return in 2025, outperforming the Swiss Performance Index by 5.9 percentage points, while trading liquidity improved materially, with average daily volume rising 56% year-on-year. That combination — relative strength, improving liquidity, and stable free float — is often consistent with the early stages of institutional accumulation, even if the name remains underfollowed by the broader market.

Crucially, this is not a high-beta momentum bank. It is a quality compounder with a defensive statistical profile: a 3.3% dividend yield, a 51.1% payout ratio, a market capitalisation of approximately CHF 2.6 billion, and continued franchise momentum reflected in assets under management growth of 12.2% to CHF 108.9 billion, supported by CHF 3.7 billion of net new money. It may not appear optically cheap on a simple price-to-book basis, but it remains attractive on a quality-adjusted basis, particularly given its sovereign anchor, conservative funding structure and durable client franchise.

Investment conclusion

LLB increasingly screens as a low-volatility, high-quality alpha candidate:

- Positive relative strength

- Exceptional balance-sheet quality

- Low credit tail risk

- Stable shareholder base

- Improving liquidity and tradability

- Underappreciated relative to its quality profile

Bottom line

In a noisy macro environment, LLB looks less like a cyclical bank trade and more like a mispriced quality factor exposure with embedded defensive alpha.